Accountable Care Organizations: Early Results and Future Challenges

Journal of Clinical Outcomes Management. 2014 August;21(8)

References

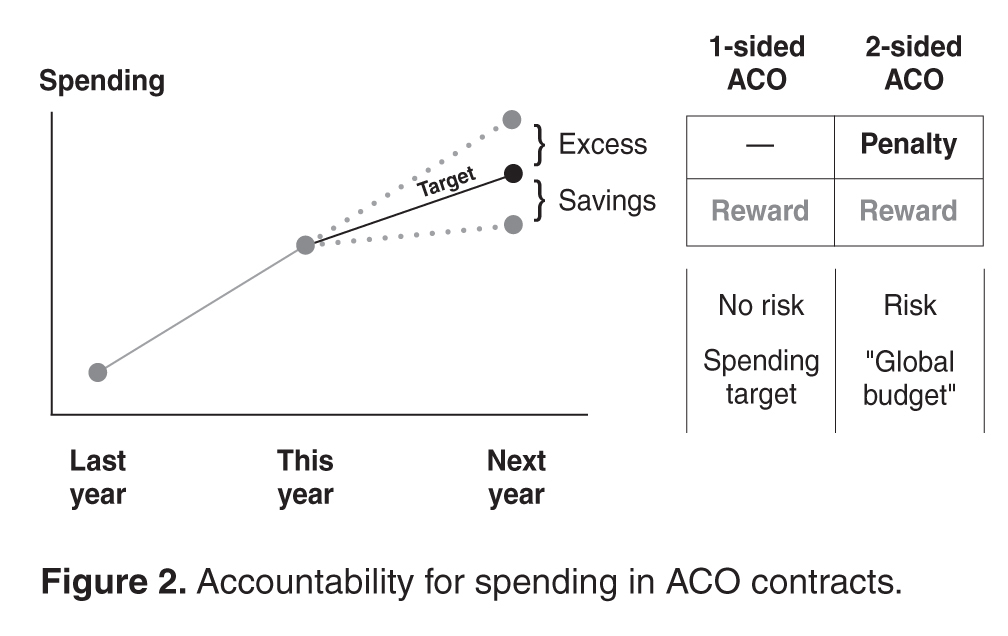

Second, an ACO takes on accountability for both spending and quality. Accountability for spending is manifested through a spending target ( Figure 2 ). Going into an ACO contract, the organization typically assumes a spending target for the upcoming year, which usually takes into account its historical cost trends and the burden of morbidity among its patients. If spending for its patient population ends up below the target by at least a minimum amount (2% in the current contract model), the organization receives a share of the savings. If spending exceeds the target by 2% or more, the organization may not be reimbursed a portion of the difference (often referred to as “downside” risk). In a so-called one-sided ACO contract—the majority of those in the Medicare Shared Savings Program—organizations face only shared savings but do not face shared risk. In two-sided contracts, such as those in the Medicare Pioneer ACO Program and many commercial ACO contracts, organizations face both shared savings and shared risk. In the latter scenario, the spending target can be appropriated called a global “budget.” Accountability for quality is operationalized through quality measurement and reporting. Using the traditional pay-for-performance framework, organizations receive bonus payments for various quality measures. In the Medicare ACO programs, for example, measures are grouped into 4 domains: (1) patient and caregiver experience, such as patients’ ratings of doctors; (2) care coordination and patient safety, such as all-cause readmission rates; (3) preventive health, such as influenza and pneumococcal vaccinations; and (4) specific measures for at-risk populations, such as hemoglobin A1c levels below 8% for patients with diabetes and beta-blockers for patients with left ventricular systolic dysfunction [17]. Accountability for quality and spending can be linked. For example, organizations may only be eligible for shared savings after they achieve a certain minimum quality performance (as in Medicare ACOs), or their shared savings and risk percentages may be tied to the level of quality (some commercial ACOs).

Third, an ACO is responsible for the care of a population of people. Each year, spending and quality are measured for the population attributed, or assigned, to the ACO. Attribution of patients to organizations can take place in two ways. It can be prospective, meaning that before the start of a contract year, the ACO knows exactly the patients whose spending and quality it is responsible for. This is typically more feasible in commercial ACO contracts, especially in the HMO population, where patients designate a primary care physician at the beginning of the year. Otherwise, attribution is typically retrospective, such as in the Medicare ACO programs, where beneficiaries are assigned to organizations at the end of a contract year based on the organization which accounted for the plurality of a patient’s medical spending or primary care spending.

Evidence to Date

While formal results from most ACOs today are not yet available, several notable ACO experiments have been evaluated. These include early results from the Medicare ACO programs, previous evaluations of the Medicare Physician Group Practice Demonstration (a predecessor of today’s ACO contracting model), and early results from commercial ACO contracts, such as the Blue Cross Blue Shield of Massachusetts global budget contract.